If a central bank sets its target rate to anything greater than zero, it further exacerbates inequality, causing millions to become (or remain) unemployed, while at the same time, giving the already-rich even more risk-free interest income.

This post describes how and why this is true, first providing a brief overview of how the central bank currently manages its version of inflation. Although it focuses on the United States and its central bank (the Federal Reserve), much of this applies to nations such as the US, UK, Australia, Canada, Japan, and so on: those with little to no foreign debt, and no commitment to converting their money to anything but itself. In other words, the countries with the most financial capacity and the least financial constraints.

(The information in this post comes substantially from my August 2020 interview with Joe Firestone: ELI5: What it means for the Federal Reserve to “defend its interest rate.”)

Important correction

An important correction, which is not yet integrated into this post: Rather than "a target rate above zero further exacerbates inequality" it should read "a target rate above the interest paid directly on reserves further exacerbates inequality." Currently the latter happens to be zero, but it doesn’t have to be. The Mosler-Forstater paper describes why, but I didn’t truly understand it until I read more advanced 2006 paper by Scott Forstater: Interest Rates and Fiscal Sustainability.

|

GO BACK TO ALL MMT RESOURCES

This post was last updated April 17, 2022. Disclaimer: I have studied MMT since February of 2018. I’m not an economist or academic and I don’t speak for the MMT project. The information in this post is my best understanding but in order to ensure accuracy, you should rely on the expert sources linked throughout. If you have feedback to improve this post, please get in touch. |

The central bank stabilizes prices by "defending its interest rate"

The United States Federal Reserve (the Fed) is unique among central banks in developed nations. It alone is mandated to manage not just price stability (inflation), but also the employment level (see Kelton 2020, chapter 2, note 15). Unfortunately, the Fed has decided that its primary directive is not to keep people employed but to manage inflation. It will therefore adjust the level of employment to whatever is necessary in order to avoid it. In other words, the Fed, and therefore the United States, deliberately chooses for millions of its citizens to be unemployed, choosing price stability, but only for some. (And we all know who gets do the choosing and who gets to be the chosen.)

Congress could manage prices for all by implementing the job guarantee as recommended by MMT, but instead leaves the matter entirely to the “free market” and the Federal Reserve's monetary policy. Unfortunately, it is impossible for the private-sector (for-profit businesses) to maintain full employment (Forstater 1999), primarily because for-profit businesses must remain profitable and must also compete with other businesses that too must remain profitable. In economic downturns, these companies must shed workers in order to survive, which is exactly when their workers are at most desperate for stable employment and income.

Only the central governments of economies with the most financial flexibility can maintain full employment in both good times and bad, because only they have no need for revenue or profit. In the words of PhD. economist John Harvey, “We are expecting [the private sector] to carry out a function that they are not designed to carry out” (2020).

Sources:

|

By Will Beaman. The concept is reminiscent of my May 2020 interview with Ryan Mathis, entitled There is nothing “natural” about society’s laws

Setting the interest rate target to greater-than-zero exacerbates inequality.

The primary tool central banks use to manage inflation is to choose an interest rate to target and then “defend” that rate. The FOMC board decides on a rate (largely based on the ideology and guesswork of its members). It then announces the new rate and that it stands ready to purchase Treasuries at any quantity at any time, at the new rate. Since the Fed is part of the central government, it can greatly outbid even the largest entity or investor (Tymoigne 2014).

(For a concise overview on the central bank's target rate and why it should be permanently be set to zero, see the 2005 paper by Warren Mosler and Mathew Forstater, The Natural Rate of Interest Is Zero.)

An interest rate greater than zero means banks must pay more for reserves when transacting in the interbank lending market (also called the banking reserve system). This causes banks to charge more for loans, which means companies take out fewer loans. This in turn increases the chance that the companies will shed workers, and who are the most likely to be shed but the disadvantaged and newly hired? The already unemployed and desperate-for-work will definitely not be hired, especially since they now have to compete with the ones just let go – those with obviously more, and more-recent, experience and skills. What it all means, is that when the Federal Reserve increases its interest-rate target, it always results in the disadvantaged being ejected from or further shut out of the job market. In other words, it keeps the poor, poor.

The Federal Reserve could defend its target rate by paying interest directly on reserves but they choose not to do that. As described in the Mosler-Forstater paper, the only other way to do it is to offer to sell bonds to the public. United States treasury bonds are interest bearing financial instruments that are, without exaggeration, 100% risk-free. As Warren calls them, bonds are “UBI for the rich.” In other words, a positive interest rate further enriches the rich.

Unfortunately, mainstream economics has asserted for decades that the primary cause of runaway, out-of-control inflation, is unemployment becoming too low. Because of this, the concept of full employment was long ago replaced with “maximum employment,” the latter of which means “as low as possible unemployment, as long as it does not trigger runaway inflation.” Therefore, according to this theory, it is paramount that the rate of unemployment not be allowed to drop below this threshold. That threshold is considered to be the “natural” rate of unemployment – and conversely, it is also the so-called maximum safe level of employment.

Critically, the runaway, out-of-control inflation they fear has never happened. So the rate of unemployment required in order to avoid it is anything but natural.

In December of 2018, the Federal Reserve raised its target rate by .25%, which is less than 1%. According to an analysis by Bill Mitchell, of the Fed's own press release and data, the increase was a conscious choice by the Fed to disemploy at least 1.2 million more Americans. (It also exacerbated inequality by further enriching the rich.)

.25 is almost zero. How can a number that small be so harmful? Conversely, the national debt is currently $26 trillion. How can a number that big not be harmful? Related post: Using numbers to hide real-world, mass suffering (and immorality).

Sources:

|

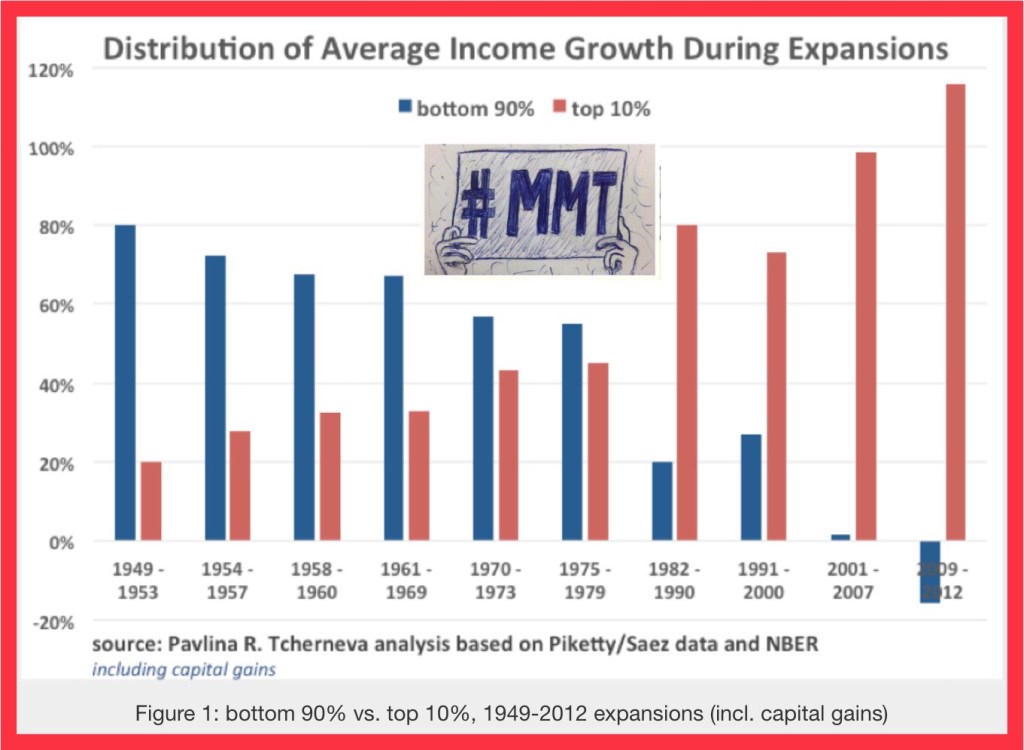

TOP IMAGE: Top image from this 2017 post by Pavlina Tcherneva, Inequality Update: Who Gains When Income Grows?