In every nation, there are three sectors in the economy: public, private, and foreign. The government alone is the public sector. Everyone and everything else in the domestic economy is the private sector (that's us!). The foreign and private sectors together are called the non-government sector. This is related to the concept of sectoral balances as developed by British economist Wynne Godley. Here is the Wikipedia entry on sectoral balances.

This post features a summary of the MMT view of sectoral balances by original MMT developer L. Randall Wray, and then another by Pakistani PhD. economist, Asad Zaman. At the bottom you will find some additional sources to learn more.

You should also read Wray's written Congressional testimony, as submitted in November 2019. It describes, through a mainstream lens, that if one wants to reduce the deficit of the government sector (or for it to have a surplus), then you must decide which other sector will be affected by that decision. However, because the United States almost always runs a trade surplus, it means that the brunt of that sacrifice will almost always be endured by the private sector. (I interviewed Dr. Wray on this paper in the second half of this episode.)

|

GO BACK TO ALL MMT RESOURCES

This post was last updated October 25, 2022. Disclaimer: I have studied MMT since February of 2018. I’m not an economist or academic and I don’t speak for the MMT project. The information in this post is my best understanding but in order to ensure accuracy, you should rely on the expert sources linked throughout. If you have feedback to improve this post, please get in touch. |

The MMT view of sectoral balances, by L. Randall Wray.

The below is an unabridged excerpt from the 2020 paper by original MMT developer, L. Randall Wray, The “Kansas City” Approach to Modern Money Theory (I interviewed Dr. Wray on this paper in this episode.):

5. SECTORAL BALANCES

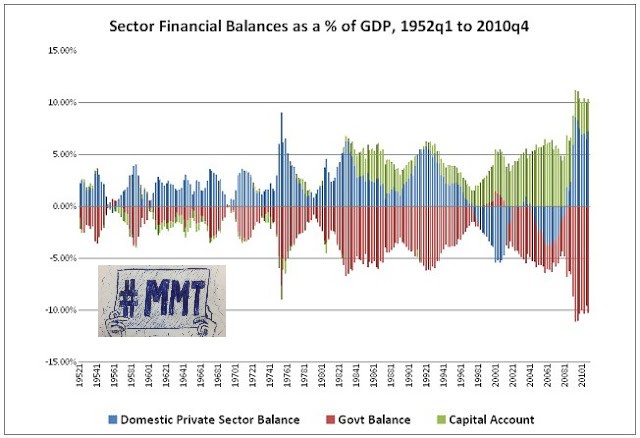

Wynne Godley arrived at the Levy Institute in the early 1990s. He began building a model of the US economy using his sectoral balance approach, with his first Levy publications coming in 1995. When I arrived for an extended stay that began in late summer of 1997, I began circulating chapters of my new book manuscript to the Levy scholars, including Wynne. At that time, Wynne was warning us about the growing deficits of the US private sector—what he would highlight in his “Seven Unsustainable Processes” paper of 1999. MMT had already included a recognition that government deficits produce surpluses for the nongovernment sectors, and government debt represents net financial wealth for the nongovernment sectors. This was a major point of Minsky's “big government” approach (discussed in the next section).

What Godley provided was a stock-flow consistent model that explicitly treated the foreign sector and that used the flow of funds accounts. This was soon added to MMT. Wynne and I collaborated on some op-ed pieces in the Financial Times and on a Levy Policy Note (Godley and Wray 1999) warning about the coming collapse of the “Goldilocks” economy. Stephanie (Bell) Kelton applied Wynne's skepticism about the future of the euro project to her own work, and I included a section in my 1998 book.28 Stephanie and Ed Nell organized a conference on the euro at the New School,29 and Warren helped to organize one in London in 1998.

The most important takeaway is that the balances must balance, meaning that we cannot think about the government's budgetary outcome independently of the other two balances. Any sector can run a surplus (the sector's income is greater than its spending), but that means at least one other runs a deficit (spending exceeds income). It is not possible to reduce the government's deficit by reducing spending or raising taxes unless the private sector's surplus declines and/or the foreign sector's surplus declines. Fiscal and monetary policy have uncertain impacts on these balances, as each balance is complexly determined and linked in complicated ways to one another. For the United States, we generally observe that robust growth is associated with a declining private sector surplus but a rising foreign sector surplus. Typically, the net result of those is a reduction of the leakages (domestic private saving and net imports), allowing the government's injection (a deficit) to fall.

But those movements of the balances also set in motion countervailing forces: the reduction of the private sector surplus generally increases debt ratios (one of Godley's most important unsustainable processes, and also highlighted by Minsky in his financial instability hypothesis; see below) even as the comovement of the government's budget toward surplus and the current account toward bigger deficits takes demand out of the economy. Once a breaking point is reached (a “Minsky moment”), a financial crisis is triggered and the fallout is accompanied by slow growth, a rising private sector surplus, falling current account deficit, and rising government deficit. Deficit hawks who want to maintain balanced budgets must explain how they are going to control the private and foreign balances to produce them.

The MMT position is that the government's balance should play the stabilizing role, accomplished by putting in place automatic stabilizers such as procyclical taxes and countercyclical spending. A deficit can certainly be too big—potentially fueling inflation. The evidence for the United States suggests that federal taxes are already sufficiently procyclical; however, if anything, federal spending is not sufficiently countercyclical, so the focus should be placed on creating a stronger movement of spending against the cycle—the topic of section seven (Wray 2019). It would also be helpful to address the inherent tendency toward financial instability in the private sector, the topic of the next section.

Asad Zaman

From his 2020 post, ABC's of Modern Monetary Theory (MMT).

Since the government is freely able to create money, it does not need to borrow any amount from the private sector. Also, at any moment of time, the government can pay off the entire debt to private sector simply by printing the required amount of money and paying it. […]

However, MMT emphatically does not say that the government SHOULD create money in arbitrary amounts. Money creation ALWAYS has economic consequences, since money is never neutral (contrary to common misconceptions created by the quantity theory of money). It is essential to consider these impacts in arriving at a decision about how much money should be created. The most important of these impacts is one which is completely absent from conventional textbooks. That is why it came as a huge surprise to me when I learned the following accounting identity from MMT texts. It is worth taking time out to understand this identity, because one cannot understand the role of government surpluses and deficits without it.

The private sector of an economy consists of households and firms. For any accounting period, like one year, let MH0 and MF0 be the amount of money held by households and firms at the beginning of the period. Let MH1 and MF1 be the amount of money in their hands at the end of the period. Then MH1-MH0 = HS is household savings over this period of time; it is the addition to their cash balances. Similarly MF1-MF0 = BP is the monetary profits of business over the year; it is the net addition to their cash balances. Now consider an economy where no money flows into or out of the private sector. Then it is clear that at the end of the year, the total amount of money will remain the same: MH0+MF0 = MH1+MF1. This can be re-written as (MF1-MF0)+(MH1-MH0)=0 or BP + HS = 0. Since the amount of money remains constant, the only way for business to make profits is if they acquire extra money from households, which requires negative savings for households. On the other hand, if households succeed in saving money, this can only happen if business as a whole makes losses, so that money is transferred from firms to households.

In a capitalist economy, firms are driven by the desire to make profits. Households are driven by the desire to save, to build up wealth as protection against future needs. The accounting identity shows that such an economy cannot function without increases in the money stock which allow both firms to make profits and households to make savings. In modern economies, there are two major sources for such injections of money into the private sector: the government and the foreign sector. First let us consider the role of the government. Taxes reduce the amount of money available in the private sector, creating greater obstacles in the path of firms seeking profits and households seeking to save: BP + HS = -T. Households will lose savings and businesses will make negative profits in order to pay taxes. Government spending into the economy (G) – whether it buys goods, invests, or pays wages, — creates additional money which is available for profits and savings. The accounting identity now becomes BP+HS = G-T. The term G-T is called the Government Deficit. This is misleading terminology borrowed from the false analogy that governments are like households and face budget constraints. The preferred term for G-T in the MMT literature is Government Injections (of money into the private sector). A capitalist economy can only function smoothly if the government continuously injects money into the economy by running deficits. The amount of the deficit must equal BP+HS – businesses can make profits, and households can create savings only if government runs deficits, creating money to allow them to do so. The overall profitability of business has nothing to do with how efficiently or competitively they run their businesses. Instead, it is bounded and partially determined by the amount of monetary injections into the economy created by government deficits.

Another way to increase the money in the economy is by foreign injections, which is (X-M). This is the money earned from sales of goods to foreigners minus the money spent on purchases from foreigners. The accounting identity for an economy with government and a foreign sector is: BP + HS = (G-T) + (X-M) which can be written out as

Business Profits + Household Savings = Government Injections + Foreign Injections

This provides us with some understanding of export led strategies for growth. If countries earn foreign exchange from exports, this can (under appropriate monetary arrangements) increase the stock of money in the domestic economy, and create the room for profits and savings to increase. However, this cannot be a preferred strategy simply because overall global exports must equal overall global imports. A monetary injection into one economy comes from a reduction in money in other economies.

Additional sources

(Will be added to. Please suggest!)

The MMT view of sectoral balances by the U.K.'s Gower Initiative for Modern Money Studies.